Want to Subscribe?

Read Corporate India and add to your Business Intelligence

![]() Unlock Unlimited Access

Unlock Unlimited Access

Published: Apr 15, 2023

Updated: Apr 15, 2023

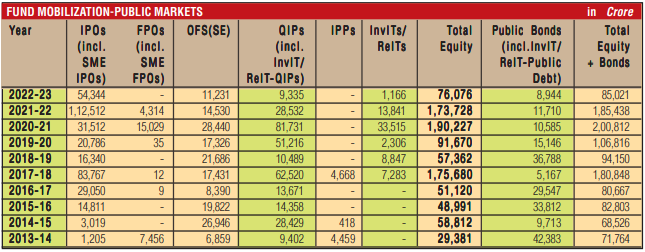

As the primary capital market was in a very bad shape during the last fiscal year ended March 2023, there was a steep fall in IPO fundraising with 37 companies raising Rs 52,116 crore through the main board, which was less than half of the Rs 1,11,547 crore mobilized by 53 companies during the previous fiscal year of 2021-22. According to Mr. Pranav Haldea, Managing Director, PRIME Database Group, Rs 20,557 crore, or a huge 39 per cent of the amount raised in 2022-23, was by LIC alone, without which the IPO fundraising would have been just Rs 31,559 crore. To be sure though, the amount raised in 2022-23 is still the third highest-ever in terms of IPO fund- raising.

Overall, public equity fundraising also dropped by 56 per cent to Rs 76,076 crore from Rs 1,73,728 crore in 2021-22.

The largest IPO in 2022-23, which was also the largest Indian IPO ever, was from Life Insurance Corp of India. This was followed by Delhivery (Rs 5,235 crore) and Global Health (Rs 2,206 crore). The average deal size was a high Rs 1,409 crore. According to Haldea, as many as 25 out of the 37 IPOs came in just 3 months of the year (May, November and December), which shows the volatile conditions prevalent through most of the year which are not conducive for IPO activity. In fact, the fourth quarter of 2022-23 has seen the lowest amount being raised in the last 9 years.

Only 2 out of the 37 IPOs (Delhivery & Tracxn) were from a new-age technology company (NATC), in comparison to 5 NATC IPOs raising in Rs 41,733 crore in 2021-22, pointing towards the slowdown in IPOs from this sector.

The overall response from the public, according to primedatabase.com, was moderate. Of the 36# IPOs for which data is available presently, 11 IPOs received a mega response of more than 10 times (of which 2 IPOs more than 50 times) while 7 IPOs were oversubscribed by more than 3 times. The balance 18 IPOs were oversubscribed between 1 and 3 times. The new HNI segment (Rs 2-10 lakh) saw an encouraging response with 11 IPOs receiving a response of more than 10 times from this segment.

In comparison to 2021-22, the response of retail investors also moderated. The average number of applications from retail dropped to just 5.64 lakh, in comparison to 13.32 lakh in 2021-22 and 12.73 lakh in 2020-21. The highest number of applications from retail were received by LIC (32.76 lakh) followed by Harsha Engineers (23.86 lakh) and Campus Activewear (17.27 lakh).

The amount of shares applied for by retail by value (Rs 41,671 crore) was 20 per cent lower than the total IPO mobilisation (in comparison to being 17 per cent higher in 2021-22), showing the lower level of enthusiasm from retail during the period. The total allocation to retail, however, was Rs 14,308 crore, which was 28 per cent of the total IPO mobilisation (up from 20 per cent in 2021-22).

According to Haldea, IPO response was further mutedby moderate listing performance. Average listing gain (based on closing price on listing date) fell to 9.74 per cent, in comparison to 32.59 per cent in 2021-22 and 35.68 per cent in 2020-21. Of the 36$ IPOs which have got listed thus far, 16 gave a return of over 10 per cent. DCX Systems gave a stupendous return of 49 per cent, followed Harsha Engineers (47 per cent) and Electronics Mart (43 per cent). 21 of the 36 IPOs are trading above the issue price (closing price of 24th March, 2023).

2022-23 saw 68 companies filing their offer document with SEBI for approval (in comparison to 144 in 2021-22), including the first ‘pre-filing’ case of Tata Play in December 2022. On the other hand, 37 companies looking to raise nearly Rs 52,060 crore let their approval lapse in 2022-23, 12 companies looking to raise Rs 10,386 crore withdrew their offer document and SEBI returned the offer document of a further 9 companies looking to raise Rs 20,330 crore.

The pipeline still remains strong. 54 companies proposing to raise a huge Rs 76,189 crore are presently holding SEBI approval. Another 19 companies looking to raise about Rs 32,940 crore are awaiting SEBI approval (out of these 73 companies, 4 are NATCs which are looking to raise roughly Rs 8,100 crore). According to Haldea, though, with weakness still prevailing in the secondary market because of a combination of domestic and foreign factors, IPO activity is likely to remain muted for the first couple of quarters. We may see some smaller- sized IPOs. However, it will be a while before we see larger-sized deals, especially in light of a lack of sustained interest from FPIs.

SME IPOs: Activity in this segment saw a huge increase in financial year 2022-23 with 125 SME IPOs collecting a total of Rs 2,229* crore in comparison to 70 IPOs in 2021-22 which collected Rs 965 crore. The largest SME IPO was of Rachana Infrastructure (Rs 72 crore).

OFS (SE): According to primedatabase.com, Offers for Sale through Stock Exchanges (OFS), which is for dilution of promoters’ holdings, saw a decrease from Rs 14,530 crore raised in financial year 2021-22 to Rs 11,231^ crore raised in 2022-23. Of this, the Government’s divestment accounted for Rs 9,522 crore or 85 per cent of the overall amount. The largest OFS was that of Axis Bank (Rs 3,876 crore). OFS accounted for 15 per cent of the year’s public equity markets mobilization.

QIPs: 11 companies mobilized Rs 8,119$ crore through QIPs during financial year 2022-23. This was 72 per cent lower than Rs 28,532 crore raised in 2021-22. The largest QIP of 2022-23 was from Macrotech Developers raising Rs 3,547 crore, accounting for 44 per cent of the total QIP amount. QIPs were dominated by real estate and financial services companies, with them accounting for 85 percent (Rs 6,887 crore) of the overall amount. In addition, there was one QIP of an Infrastructure Investment Trust (InvIT) of National Highways Infra Trust of Rs1,216 crore.

InvITs/ReITs: The amount raised through InvITs and ReITs saw a huge decrease of 92 per cent to just Rs 1,166 crore from Rs 13,841 crore in 2021-22.

Fresh Capital: Of the total equity mobilisation of Rs 76,072 crore, fresh capital amount was Rs 22,985 crore (30 per cent), the remaining Rs 53,087 crore being offers for sale.

Divestments: Divestment in financial year 2022-23 was dominated by the mega IPO of LIC which contributed Rs 20,557 crore of the total divestment amount of Rs 31,050 crore (66 per cent) raised by the Government. Public Offers (IPOs of LIC, Paradeep Phosphates and OFS of Axis Bank (SUUTI), HAL, IRCTC and ONGC at Rs 30,552 crore (98 per cent) were the most used mode followed by Buyback (GAIL) at Rs 498 crore (2 per cent).

Rights Issues: Mobilisation of resources through rights issues, according to primedatabase.com, stood at just Rs 5,779 crore in financial year 2022-23, which was 77 per cent lower than Rs 25,301 crore that was raised in 2021-22. The largest Rights Issue of 2022-23 was from Capri Global raising Rs 1,440 crore, accounting for 25 per cent of the total Rights Issues amount. By number though, the year witnessed 12 companies using the rights route in comparison to 10 companies in 2021-22.

Public Bonds: The public bonds market also saw a decrease of 30 per cent with 32 issues raising Rs 7,444 crore, in comparison to 27 issues raising Rs 10,710 crore last year. The largest issue was from Creditaccess Grameen raising Rs 500 crore. In addition, there was one Public Debt issue of an InvIT (National Highways Infra Trust of Rs1,500 crore).

Debt Private Placements: The amount raised through debt private placement in the financial year 2022-23 stood at Rs 8,03,812 crore (as on 27th March, 2023), up 27 per cent from Rs 6,34,167 crore in 2021-22. This was mobilised by 807 institutions and corporates. The highest mobilisation through debt private placements was by HDFC (Rs 78,415 crore) followed by NABARD (Rs 48,649 crore) and SBI (Rs 38,851 crore). In addition, there were 9 debt private placements from InvITs/ReITs raising Rs 4,900 crore.

Overseas Bonds: Indian companies also raised Rs 1,86,873 crore through overseas borrowing (including ECBs@), down 52 per cent from Rs 3,87,671 crore in 2021-22.

At an overall level, fundraising by Indian corporates, through equity and debt, in India and abroad, covering IPOs, FPOs, OFS (SE), Rights, QIP, InvITs/ReITs, preferential issues, Public Debt, Debt Private Placement, Overseas Bonds, ECB and FCCB, dropped by 10 per cent to Rs 11.73 lakh crore in the financial year 2022-23 from Rs 12.98 lakh crore in 2021-22.

February 15, 2025 - First Issue

Industry Review

VOL XVI - 10

February 01-15, 2025

Want to Subscribe?

Read Corporate India and add to your Business Intelligence

![]() Unlock Unlimited Access

Unlock Unlimited Access

Lighter Vein

1 Year *

Subscription

Rs 2400 /-

3 Year *

Subscription

Rs 6000 /-

5 Year *

Subscription

Rs 9000 /-

5

International

Subscription

$ 99.99

Read Corporate India and add to your Business Intelligence

Popular Stories

A modern-day enigma and a ramification of humanity's never-ending advancements, e-waste refers to the scum con- cealed by the outward glow of ever-advancing technology.

Archives

Office Address

Unit No. 405, 4th floor, Madhu Industrial Park, Avadh Narayan Tiwari Marg, Mogra Village Road, Andheri (East), Mumbai – 400069.

Call/Whatsapp

If you are interested in advertising with Corporate India, please don't hesitate to contact us. Our team is here to assist you with the process and answer any questions you may have. We look forward to the opportunity to work with you and help your business reach its full potential.

Fill out the form below to subscribe to our newsletter and never miss an update