Want to Subscribe?

Read Corporate India and add to your Business Intelligence

![]() Unlock Unlimited Access

Unlock Unlimited Access

Published: April 15, 2024

Updated: April 15, 2024

Boomtime beckons the $ 500 billion Indian healthcare industry on the back of several favourable factors, among them a huge population, a ‘readymade client’ population of 100 million seniors, the fastest growing economy in the world, increasing middle class spending, growing lifestyle diseases and increased health insurance coverage.

In fact, experts predict that the domestic healthcare market will surpass $ 1,000 billion over the next decade.

Hospitals are clearly the biggest and most visible segment of the healthcare industry, and their growth – anticipated at $ 155 billion by 2032 — is being fuelled by the government as well as the private sector, with foreign investors waiting in the wings to cash in on the domestic demand for hospitals.

Other growth engines in the healthcare sector are medical devices, medical tourism, health insurance, biotech & biopharma, and digital healthcare.

The $ 500 billion Indian healthcare industry – one of the largest sectors of the Indian economy – is on a roll. It is growing at a brisk pace, thanks to its expanding nationwide coverage and increasing expenditure by both the public and private sectors. Over the last decade, the sector has become increasingly visible, thanks to the renewed focus from the government and the growing demand for healthcare services and products. Pertinently, the Indian population is growing at a rate of 1.6 per cent and the country has already overtaken China as the most populous country in the world. Moreover, India has an elderly population of over 100 million, a readymade market for the healthcare industry.

Among other factors favouring the rapid growth of the sector are the country’s emergence as the fastest growing economy in the world with a GDP growth of around 7 per cent, rising middle class incomes, improving standard of life and growing lifestyle diseases, and increased market penetration of health insurance services. In addition, a shift from chronic to lifestyle diseases has led to a boom in government healthcare spending.

According to NextGen, the Indian healthcare industry hit the $ 500 billion mark this year and is expected to reach $ 610 billion by 2026. Some experts anticipate the market size to cross $ 1,000 billion within the next 10 years. This remarkable spurt in market size is attributed to the fast growing demand for specialized and higher quality healthcare facilities and services. The products, services and segments driving this growth include hospitals, medical devices, clinical trials, digital healthcare and telemedicine, medical tourism, health insurance, and medical as well as diagnostic equipment. The rapid growth of all these segments is fuelled by large investments from the government and corporate hospital chains, and new investments backed by private equity investors

Needless to say, the most visible segment of the healthcare industry is hospitals. In India, healthcare is provided through primary, secondary and tertiary care hospitals. The first two categories —primary and secondary — are fully managed by the government, while tertiary hospitals are owned and managed by either the government or private companies. Though the private sector’s has entered relatively late, its contribution to the healthcare sector has been growing at a faster pace than that of the government. What is more, hospitals are being established in the corporate sector too, with joint sector companies raising funds from the public to set up hospitals. Of late, the medical infrastructure market has been growing at an estimated 15 per cent annually. Interestingly, the importance of hospitals is on the rise and both the government and the private sector are planning to set up several new speciality hospitals as well as to modernise existing hospitals.

Inspite of this trend, the rising population and the increasing awareness about the necessity for medical treatment has led to a chronic shortage of healthcare infrastructure, especially in two- and three-tier cities and rural areas. According to current estimates, India will require upto 175 million more hospital beds by the end of 2025 — creating an opportunity for foreign companies to set up hospitals in the country through the FDI route. At present, India’s hospital industry is growing at a compounded annual growth rate of over 5.75 per cent and is expected to reach $ 155 billion by 2032.

The Indian government regulates medical devices (including instruments, implants, and software intended for human or animal medical use) as ‘drugs’ under the Drugs & Cosmetics Act (D&C Act), 1940. In July 2022, the Ministry of Health and Family Welfare (MoHFW) unveiled a new bill intended to replace the D&C Act, so as to increase safety, effectiveness, and alignment with global standards of medical devices, drugs, and cosmetics available in India. The draft bill is expected to be presented during the upcoming parliamentary proceedings. Once approved by the Parliament, the new bill will provide a regulatory regime governing medical devices, pharmaceuticals and cosmetics in India.

In May 2023, the government introduced a National Medical Device policy, whose goals are: achieving universal access to quality medical devices; boosting domestic manufacturing capacity for affordability; enhancing product quality and global competitiveness; improving clinical outcomes through early diagnosis and accurate treatment; promoting a healthier lifestyle through extensive device applications; fostering innovation in the sector, and developing strong local manufacturing capabilities and resilient supply chains. The policy also aims to streamline regulation, enabling infrastructure, R&D and innovation to facilitate the sector’s growth and development.

In January 2022, the Indian government issued a notification requiring all medical device companies to register their devices with the Central Drugs Standard Control Organization in compliance with a mandatory ISO 13485 certification. This requirement is designed to ensure the safe production and control of medical devices and in-vitro diagnostic products. Previously, medical devices were subject to a voluntary registration scheme. Starting in October 2021, Class A and B medical devices were subject to mandatory registration, and from September 2022, Class C and D medical devices are subject to mandatory registration. After the expiry of the mandatory registration period in September 2023, these medical device classes are to transition to a licensing regime.

The Indian medical tourism market is growing at a fast pace. According to the 'India Tourism Statistics At A Glance' 2020 report, close to 6,97,300 foreign tourists came for medical treatment in India during fiscal year 2019. The medical tourism market, valued at $ 2.89 billion at that time (2019- 2020), has reached $ 7.09 billion in fiscal 2024 and is expected to touch $ 14 billion mark by 2029.

By now, India has became a popular destination for medical tourism due to its advanced healthcare facilities, skilled healthcare professionals, and lower costs of medical treatment compared to developed countries. The Indian medical tourism market offers various medical services, including cardiac surgery, organ transplantation, cosmetic surgery, dental care, and traditional medicine. The Indian government has implemented various policies and initiatives to promote medical tourism, such as streamlining visa processes and developing specialized medical tourism zones. In addition, India has a large pool of English-speaking doctors and nurses, which makes it easier for patients from English-speaking countries to communicate with their healthcare providers. Little wonder, India is ranked among the top 10 in the medical tourism index out of around 50 destinations by the Medical Tourism Association. With a $ 7.69 billion tourism market size and 500,000 international patients annually, India is today among the top global destinations for international patients seeking advanced treatment.

Medical care in India is provided 'at cost' and most Indians pay out-of-pocket since they fall outside insurance schemes, which makes healthcare out of reach for many. Health insurance is gaining momentum, with 30 per cent of the population covered by government insurance and private insurance. Several private insurance companies have entered the market and have petitioned hospitals to provide cashless treatment to subscribers of insurance companies. Biotech and biopharma: Biotech and biopharma are two fast-growing segments of the Indian life sciences sector and represent diverse opportunities for US companies. The Indian biotech industry comprises over 800 companies and has a market size of $ 80 billion, constituting approximately three per cent of the global biotech industry. India is also a leading destination for clinical trials, contract research, and manufacturing in this sector.

Though in its infancy, digital healthcare and telemedicine have expanded rapidly since the onset of the Covid-19 pandemic. People are adapting to new health technologies and intelligent solutions to reduce barriers between hospitals and patients. Telemedicine technology and artificial intelligence will provide significant opportunities for US firms in the coming years. Several major Indian players such as Apollo, AIIMS, and Narayana Hrudayalaya have adopted telemedicine services. The Ministry of Health and Family Welfare along with NITI Aayog, the Indian government's public policy think tank, have recently released official guidelines for telemedicine practices that allow registered medical practitioners to provide remote consultation under the supervision of the National Medical Commission, formerly known as on the Medical Council of India.

It can thus be seen that India's healthcare sector is extremely diversified and at the same time has opportunities aplenty in every segment. To keep abreast of the mounting competition, businesses are looking to explore the latest dynamics and trends. One proof of this is the hospital segment which is expected to grow to $ 200 billion (Rs 12.72 trillion) by fiscal year 2025 from $ 1.79 billion (Rs 4 trillion) in fiscal year 2017.

In the medical devices segment, India is a land of opportunities. Despite the government's 'Make in India' initiatives, this segment heavily reliant on imports in areas like diagnostic kits, reagents and hand-held diagnostic equipment. Almost 50 per cent of these products are at present imported, creating huge opportunities for players in the space of import substitution. Interestingly, Indians today are getting more and more health-conscious. Growing urbanization, rising income levels, an ageing population, and changing attitudes towards preventive healthcare are expected to boost the demand for healthcare services in the future. Greater health insurance coverage has added to the rise in healthcare spending, a trend that is likely to intensify going ahead.

The Indian medical tourism market is expected to grow immensely going ahead. The government aims to develop India as a global healthcare hub and is planning to increase public health spending to 2.5 per cent of the country's GDP by 2025. Little wonder that India's healthcare industry is set for boomtime in the coming years. The diversity of India's healthcare sector means there are opportunities aplenty in every segment. There are around 70,000 hospitals in the country, of which 45,000 belong to the private sector, outnumbering the public sector's 25,000 hospitals. Among the private sector hospitals, around 50 hospital companies are listed on the stock exchanges. Most of these companies are doing quite well and their prices have tended to move up for the following reasons:

Apollo Hospitals Enterprise (Apollo), which is rated one of Asia's best private healthcare providers, has a solid presence in every sector of the healthcare market, including primary care facilities, pharmacies, hospitals and diagnostic clinics. The company has made rapid strides on the financial front. During the last 12 years, its sales turnover has grown more than five times - from Rs 3,148 crore in fiscal 2012 to Rs 16,612 crore in fiscal 2023, with operating profit shooting up almost four times from Rs 517 crore to Rs 2,065 crore and the profit at net level also surging around four times from Rs 218 crore to Rs 844 crore. It is anticipated that Apollo will see annual growth in earnings and sales of 35.9 per cent and 15.2 per cent respectively. An annual growth rate of 36.5% is projected for EPS and a 20.9% return on equity in 3 years.

Sikandarabad (Telangana)-based Krishna Institute of Medical Sciences (KIMS) is a renowned healthcare institution known for its excellent financial performance as it provides extensive healthcare services spanning many cities. During the last half-century, it has emerged as a leading corporate healthcare organization in Telangana and Andhra Pradesh by providing specialized treatment across various departments and institutes. The company has put up an excellent show on the financial front. During the last eight years, its sales turnover has spurted more than four times - from Rs 512 crore in fiscal 2016 to Rs 2,198 crore in fiscal 2023, with operating profit shooting up more than five times - from Rs 109 crore to Rs 599 crore, and the profit at net level taking a 13-fold high jump -- from Rs 28 crore to Rs 366 crore.

Max Healthcare Institute Ltd is considered one of the most forward looking and innovative healthcare providers in the country, offering a comprehensive range of services and a solid financial foundation. The company is a highly profitable private hospital organization with more than 4,800 physicians and more than 3,600 beds spread over 17 locations in India. The company has put up a scintilating performance on the financial front. During the last seven years its sales turnover has advanced from Rs 1,608 crore in the fiscal 2017 to Rs 4,563 crore in fiscal 2023, with operating profit registering an almost nine-fold spurt from Rs 141 crore to Rs 1,241 crore, and the net profit zooming 69 times from Rs 16 crore to Rs 1,104 crore.

Rated as the most investor-friendly healthcare company, Aster DM Healthcare gives its shareholders a return of 70- 80 per cent of the profits, which may result in dividends of Rs 110-120 per share. Of late, the company has sold its Gulf division to Alpha GCC Holdings Ltd for $ 1.01 billion, and the proceeds of the deal will be utilized for expansion, among other things. The company has planned to add 1,500 beds to its multispeciality medical centres throughout India. The company has budgeted between Rs 800-850 crore for this purpose. The company has put up a gratifying show on the financial front. During the last 11 years, its sales turnover has reported a six-fold spurt from Rs 1,922 crore in fiscal year 2013 to Rs 11,933 crore in fiscal 2023, with operating profit shooting up more than six times from Rs 261 crore to Rs 1626 crore and the net profit more than trebling from Rs 149 crore to Rs 475 crore.

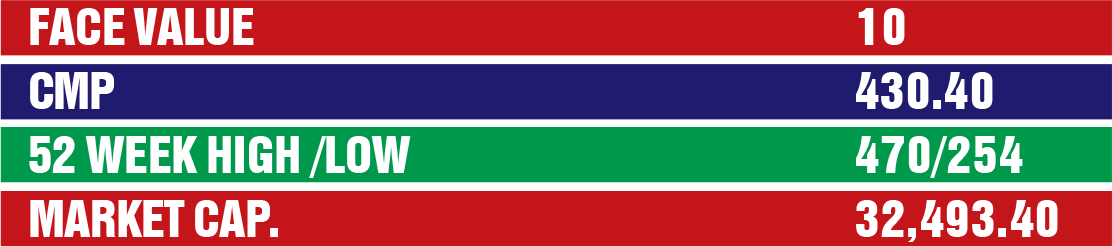

Rated one of the best hospital chains in India, Fortis Healthcare's hospitals are located in Mumbai, Delhi, Chennai, Chandigarh, Bengaluru, Kolkata and Navi Mumbai, among others. Malaysia's IHH HealthCare has got the controlling stake in Fortis after the former acquired a 31 per cent stake in the company. Four IHH Healthcare representatives have been appointed on the Fortis board and they control the management. Reflecting its dedication to sustainable growth, Fortis Healthcare Ltd is committed to growth and diversification, preserving its position as the nation's top diagnostic brand in Tier 2 and 3 markets. The company is doing well on the financial front. During the last 12 years, its sales turnover has expanded from Rs 2,618 crore in fiscal 2012 to Rs 6,298 crore in fiscal 2023, with operating profit shooting up from Rs 328 crore to Rs 1,101 crore and the net profit surging ahead from Rs 67 crore to Rs 633 crore. Fortis Healthcare has a P/E ratio 57.28 as compared to the sectoral P/E of 28.33. There are 11 analysts who have initiated coverage on Fortis Healthcare. There are 3 analysts who have given it a strong 'buy' rating and 8 analysts who have given it a 'buy' rating. No analyst has given the stock a 'sell' rating.

February 15, 2025 - First Issue

Industry Review

VOL XVI - 10

February 01-15, 2025

Want to Subscribe?

Read Corporate India and add to your Business Intelligence

![]() Unlock Unlimited Access

Unlock Unlimited Access

Lighter Vein

1 Year *

Subscription

Rs 2400 /-

3 Year *

Subscription

Rs 6000 /-

5 Year *

Subscription

Rs 9000 /-

5

International

Subscription

$ 99.99

Read Corporate India and add to your Business Intelligence

Popular Stories

A modern-day enigma and a ramification of humanity's never-ending advancements, e-waste refers to the scum con- cealed by the outward glow of ever-advancing technology.

Archives

Office Address

Unit No. 405, 4th floor, Madhu Industrial Park, Avadh Narayan Tiwari Marg, Mogra Village Road, Andheri (East), Mumbai – 400069.

Call/Whatsapp

If you are interested in advertising with Corporate India, please don't hesitate to contact us. Our team is here to assist you with the process and answer any questions you may have. We look forward to the opportunity to work with you and help your business reach its full potential.

Fill out the form below to subscribe to our newsletter and never miss an update