Want to Subscribe?

Read Corporate India and add to your Business Intelligence

![]() Unlock Unlimited Access

Unlock Unlimited Access

Published: June 15, 2024

Updated: June 15, 2024

This fortnight we have selected Data Patterns (India), the brainchild of Srinivasagopalan Rangarajan, which has during its existence of around four decades emerged as a leading player in the fields of defence and aerospace. The Chennai-headquartered company specialises in designing and solutions. With a focus on indigenous development in line with the government's 'Make in India' policy stance, the company offers a range of products that cater to the entire spectrum of defence and aerospace (land, sea, air and space) platforms. It has a 100 per cent in-house development and manufacturing capacity with a diversified order book and marquee customers. It has supplied products for LCA-Tejas, the light utility helicopter and the Brahmos missile.

Today, the company stands out in the defence and aerospace electronics segment with a wide range of diversified products. Its product portfolio includes: (1) radar, including surveillance radar (which detects moving targets), weather radar (specialized for cloud and rainfall measurement), wind profile radar (which helps in determining the direction and intensity of the wind at various altitudes), tracking radar (used by satellites to monitor the flight trajectory), and Brahmos missile seeker; (2) electronic warfare (EW), including systems for electronic support; (3) avionics display (used in cockpits of aircraft and helicopters); (4) automated test equipment (used in electronic devices for functionality and performance).

The diversity of the company's product range shows its ability to cater to a wide spectrum of requirements in the defence and aerospace sectors.

The company has three diverse revenue streams: (1) Service (providing support and maintenance services) for electronic systems and sub-systems; (2) Development (design and development of phase of a new product or customizing an already existing product to specific client needs; (3) Production (actual manufacturing and sale of the company's products).

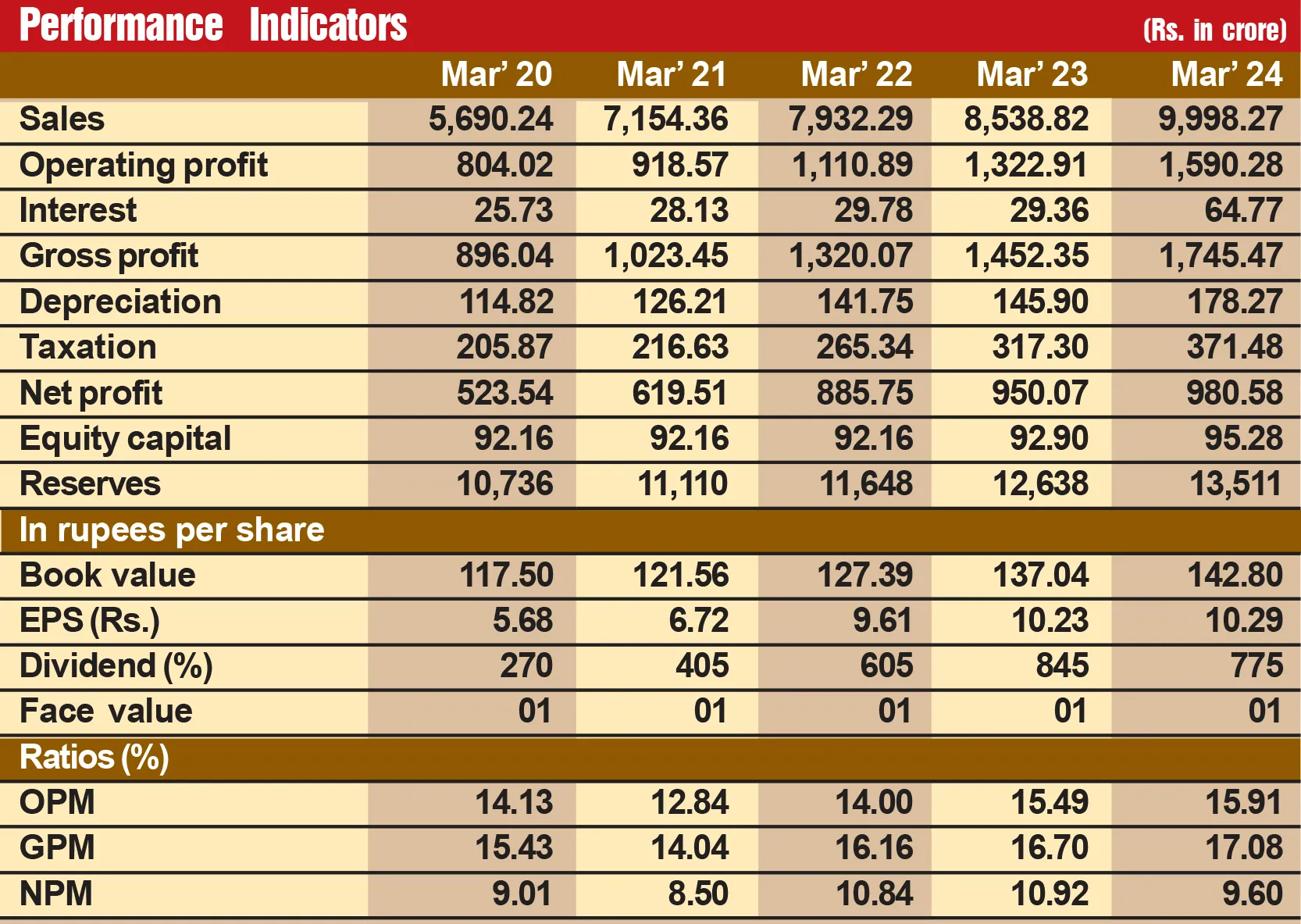

Demand for the company's products is on the rise and as a result its financial performance is steadily improving. During the last 11 years, its sales turnover has expanded by over eight times from Rs 63 crore in fiscal 2014 to Rs 520 crore in fiscal 2024, with operating profit shooting up over 13 times from Rs 17 crore to Rs 222 crore and the profit at net level taking a 26-time high jump - from Rs 7 crore to Rs 182 crore. What is more, visible trends indicate that prospects for the company are all the more promising going ahead. Consider:

Discerning investors will do well to accumulate these stocks at every decline, as the stock is fundamentally very strong and its future prospects are highly promising.

February 15, 2025 - First Issue

Industry Review

VOL XVI - 10

February 01-15, 2025

Want to Subscribe?

Read Corporate India and add to your Business Intelligence

![]() Unlock Unlimited Access

Unlock Unlimited Access

Lighter Vein

1 Year *

Subscription

Rs 2400 /-

3 Year *

Subscription

Rs 6000 /-

5 Year *

Subscription

Rs 9000 /-

5

International

Subscription

$ 99.99

Read Corporate India and add to your Business Intelligence

Popular Stories

A modern-day enigma and a ramification of humanity's never-ending advancements, e-waste refers to the scum con- cealed by the outward glow of ever-advancing technology.

Archives

Office Address

Unit No. 405, 4th floor, Madhu Industrial Park, Avadh Narayan Tiwari Marg, Mogra Village Road, Andheri (East), Mumbai – 400069.

Call/Whatsapp

If you are interested in advertising with Corporate India, please don't hesitate to contact us. Our team is here to assist you with the process and answer any questions you may have. We look forward to the opportunity to work with you and help your business reach its full potential.

Fill out the form below to subscribe to our newsletter and never miss an update