Want to Subscribe?

Read Corporate India and add to your Business Intelligence

![]() Unlock Unlimited Access

Unlock Unlimited Access

Published: March 15, 2023

Updated: March 15, 2023

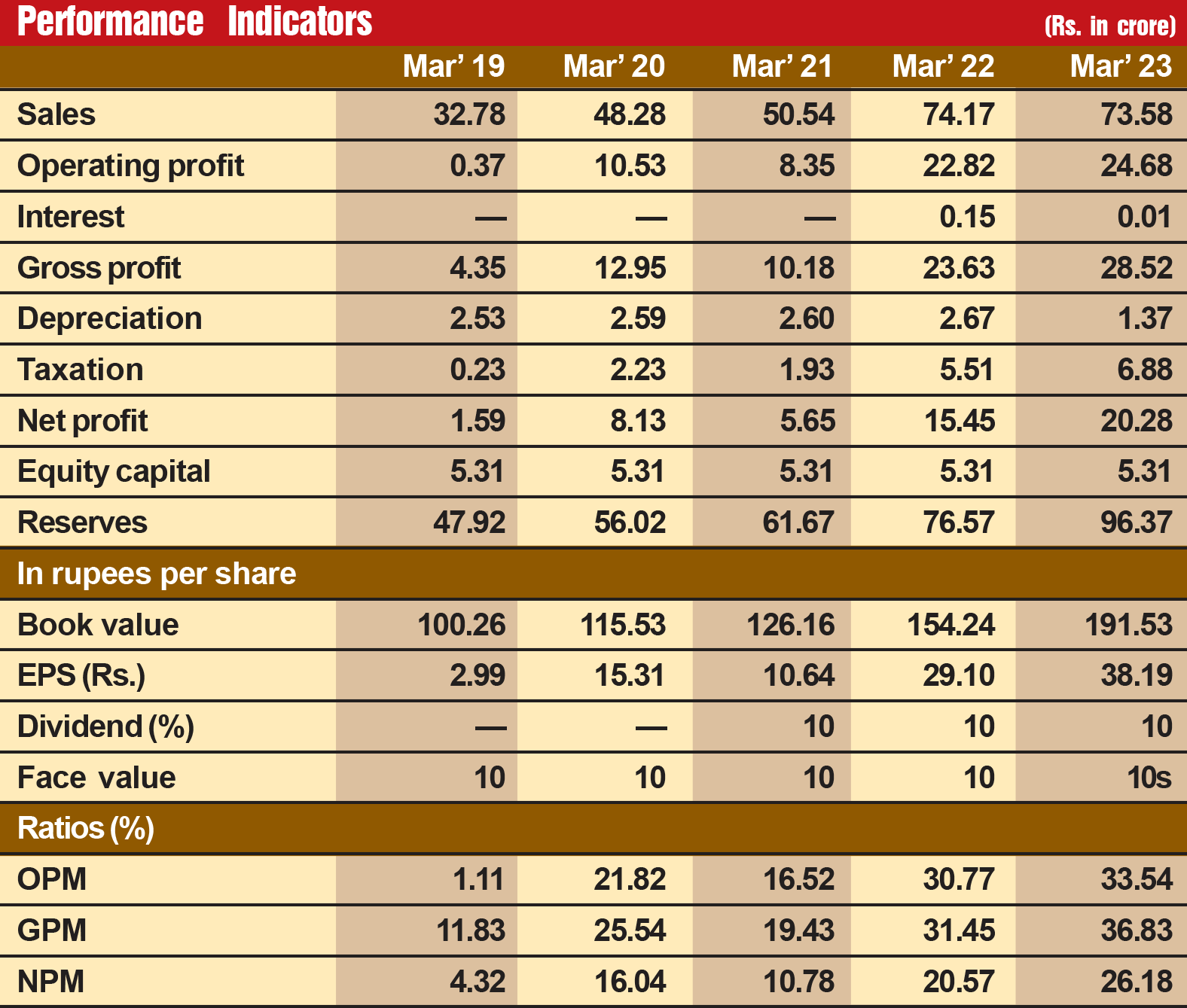

This fortnight, we have selected a unique small cap multinational company (equity capital Rs 5 crore, market capitalisation Rs 860 crore). This little-known company is De Nora India, a subsidiary of the De Nora group of The Netherlands. In fact, the parent company was founded by Italian engineer Oronzio De Nora in 1923. Subsequently, the company promoted subsidiaries and joint ventures throughout the world. Today, there are 25 operating companies in 10 countries. Five R&D centres in Italy, the US and Japan ensure continuous improvement and enlargements of its proprietary technology covered by about 260 patent families with over 2,700 territorial extensions. The company’s subsidiaries are in Italy, Germany, The Netherlands, Europe, the US, Canada, Japan, Singapore and China, and De Nora serves customers in more than 100 countries.

In 1988, De Nora decided to enter India and joined hands with an Indian promoter group headed by the then Managing Director of Alfa Lavel. The next year, in late 1989, it formed a company styled Titanor Components Ltd, which acquired the metal anode division of Wimco located in Parwana village, Rampur (UP). As the volume of business started growing, the company set up a state-of-the-art plant in Kundaim, Goa and started meeting the demands of the rapidly developing chlor-alkali industry. Subsequently, the name of the company was changed to De Nora India. Its strength lies in its technical expertise backed by well-trained specialists who are supported by the parent’s highly qualified engineering staff.

The company began on a highly promising note but in the first decade of the new millennium started faltering as promoter Devika Khanna’s ‘arbitrary’ actions dismayed the parent company, which refused to supply technology and other support. As a result, the company’s performance started deteriorating. The sales turnover dropped to Rs 30-40 crore, and operating profit, which dropped to Rs 7 crore in fiscal 2011, nosedived further to zero in 2019.

The company’s future seemed bleak, but fortunately for it the Indian promoter was declassified as promoter. There was no go but to sell the shares of De Nora India at a price of Rs 250 in the market, and thus the parent company with a 54 per cent equity stake took full control of the management. Technological and other support were restored and the company returned to the growth path. During the last five years, its sales turnover has more than doubled from Rs 33 crore in fiscal 2019 to Rs 74 crore in fiscal 2023, with operating profit shooting up from zero to Rs 25 crore and the profit at net level surging from Rs 2 crore to Rs 15 crore.

The Indian subsidiary was not only ensured a regular flow of technology but was also now able to seamlessly import knocked down kits, components and spares on credit from De Nora subsidiaries worldwide. As the company started doing well, its share price started jumping up to reach an alltime high of Rs 2,334 before settling at around Rs 1,630. We have picked De Nora for our Fortune Scrip status this fortnight as the worst is over for the company after Devika Khanna of the Indian promoter group left the company. Now, the company is on a steady growth path. What is more, with green hydrogen getting a lot of importance in the country's energy policy, prospects for De Nora have brightened all the more. Consider:

February 15, 2025 - First Issue

Industry Review

VOL XVI - 10

February 01-15, 2025

Want to Subscribe?

Read Corporate India and add to your Business Intelligence

![]() Unlock Unlimited Access

Unlock Unlimited Access

Lighter Vein

1 Year *

Subscription

Rs 2400 /-

3 Year *

Subscription

Rs 6000 /-

5 Year *

Subscription

Rs 9000 /-

5

International

Subscription

$ 99.99

Read Corporate India and add to your Business Intelligence

Popular Stories

A modern-day enigma and a ramification of humanity's never-ending advancements, e-waste refers to the scum con- cealed by the outward glow of ever-advancing technology.

Archives

Office Address

Unit No. 405, 4th floor, Madhu Industrial Park, Avadh Narayan Tiwari Marg, Mogra Village Road, Andheri (East), Mumbai – 400069.

Call/Whatsapp

If you are interested in advertising with Corporate India, please don't hesitate to contact us. Our team is here to assist you with the process and answer any questions you may have. We look forward to the opportunity to work with you and help your business reach its full potential.

Fill out the form below to subscribe to our newsletter and never miss an update