Want to Subscribe?

Read Corporate India and add to your Business Intelligence

![]() Unlock Unlimited Access

Unlock Unlimited Access

Published: March 31, 2024

Updated: March 31, 2024

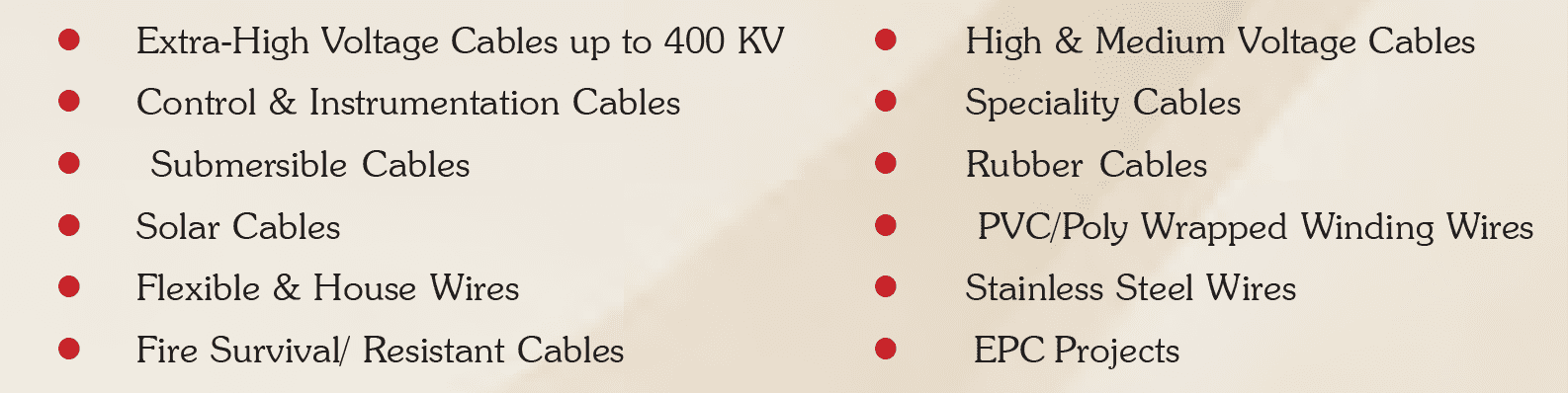

This fortnight we have selected a prominent wire and cables company as the Fortune Scrip. Incorporated way back in 1968, New Delhi-headquartered Krishna Electric Industries, which began life as a small partnership firm, has during the last five decades blossomed into a global empire (listed as KEI Industries on the stock exchanges) that provides comprehensive wire and cable solutions through a vast network of over 30,000+ channel partners. The company, which initiated its journey in 1968 with a primary focus on the production of rubber cables for house wiring, can boast today of a wide range of of over 400 products, including:

With these products and capabilities, the company serves a wide spectrum of sectors such as power, oil refineries, railways, automobiles, cement, steel, fertilizers, textile and real estate.

KEI is much more than just a cables and wires producer. It is an industry and market leader in India and a chosen supplier to both private and public sector clients worldwide. It is an end-to-end solutions provider with a product line-up that includes every type of cable and wire created to meet the unique and niche needs of its diverse clients in the retail, institutional (EHV+EPC) and exports segments.

The company has made investments in expanding its capabilities and constructing flexible manufacturing facilities over the years, positioning itself to take advantage of opportunities arising from power utility, core infrastructure, industrial and building and construction projects around the nation. The prospective horizon is further broadened by its judicious entry into the EHV cable segment and EPC services for power sector projects.

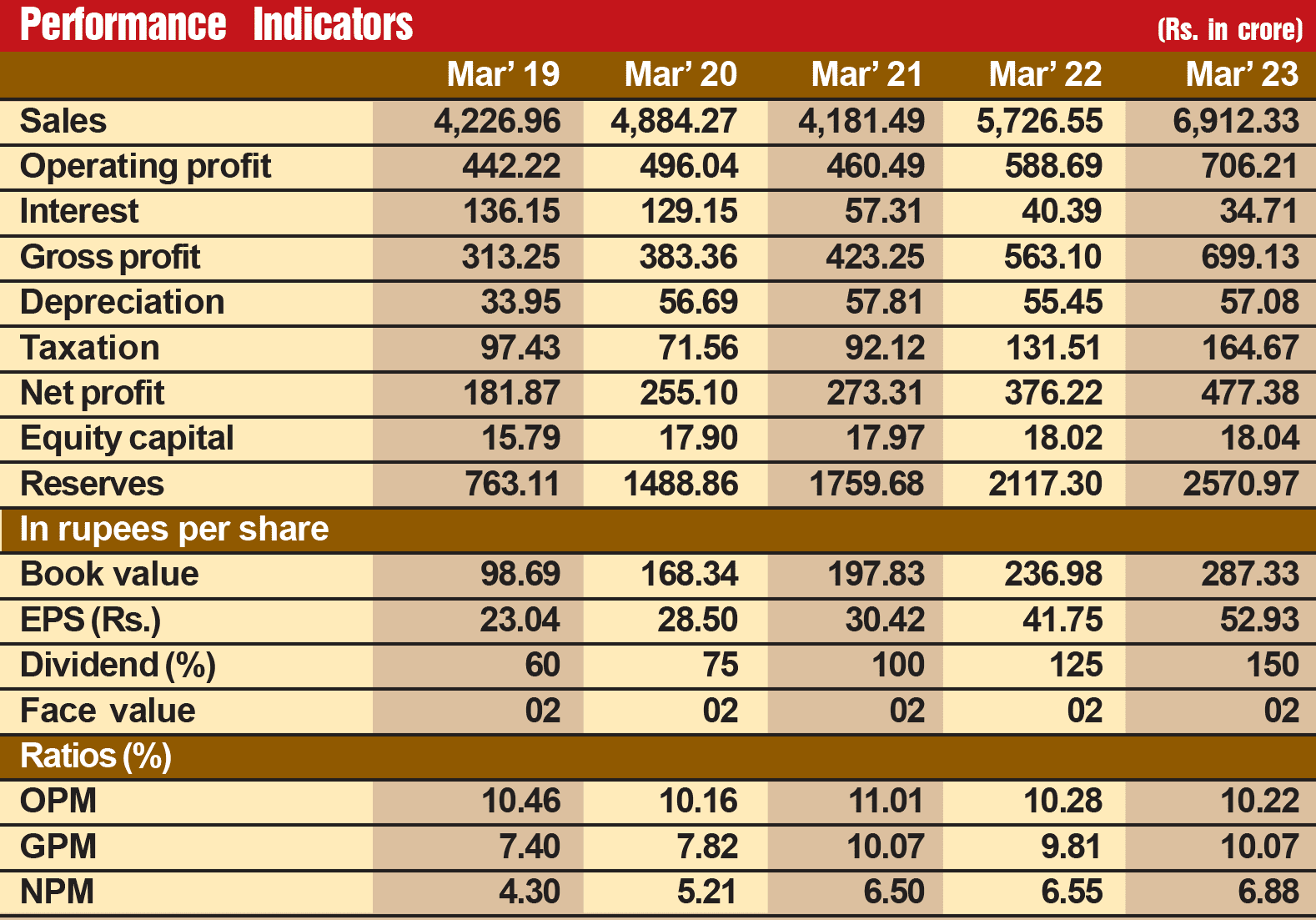

KEI has been steadily growing on the financial front. During the last 12 years, its sales turnover has increased four-fold from Rs 1,706 crore in fiscal 2012 to Rs 6,912 crore in fiscal 2023, with operating profit expanding more than four times from Rs 150 crore to Rs 706 crore and the profit at net level surging over seven times from Rs 24 crore to Rs 177 crore.

However, we have not selected KEI as the Fortune Scrip on account of its past robust financial performance. We strongly feel that prospects for the company going ahead are all the more promising. Consider:

To begin with, the company plans to increase its export share, particularly in the US market, following the recent approval of its products for export to the US by fiscal 2024. The company hopes to significantly enhance its exports to the US in the coming years.

February 15, 2025 - First Issue

Industry Review

VOL XVI - 10

February 01-15, 2025

Want to Subscribe?

Read Corporate India and add to your Business Intelligence

![]() Unlock Unlimited Access

Unlock Unlimited Access

Lighter Vein

1 Year *

Subscription

Rs 2400 /-

3 Year *

Subscription

Rs 6000 /-

5 Year *

Subscription

Rs 9000 /-

5

International

Subscription

$ 99.99

Read Corporate India and add to your Business Intelligence

Popular Stories

A modern-day enigma and a ramification of humanity's never-ending advancements, e-waste refers to the scum con- cealed by the outward glow of ever-advancing technology.

Archives

Office Address

Unit No. 405, 4th floor, Madhu Industrial Park, Avadh Narayan Tiwari Marg, Mogra Village Road, Andheri (East), Mumbai – 400069.

Call/Whatsapp

If you are interested in advertising with Corporate India, please don't hesitate to contact us. Our team is here to assist you with the process and answer any questions you may have. We look forward to the opportunity to work with you and help your business reach its full potential.

Fill out the form below to subscribe to our newsletter and never miss an update