Want to Subscribe?

Read Corporate India and add to your Business Intelligence

![]() Unlock Unlimited Access

Unlock Unlimited Access

Published: November 30, 2024

Updated: November 30, 2024

Ever since Prime Minister Narasimha Rao and his Finance Minister Manmohan Singh opened up India to economic liberalisation, the domestic banking sector has grown by leaps and bounds. Private banks in particular have been the biggest beneficiaries and have outpaced their public sector counterparts.

Besides, there is an abundance of foreign banks, besides small finance banks, co-operative banks and regional rural banks. While traditional banking continues to thrive, digital payments have increased by leaps and bounds. As of July 31, 2024, there were 602 banks actively using UPI.

Monthly transactions via UPI hit 16.58 billion in October 2024, up from a few hundred million in early 2018, significantly displacing cash across the country at outlets, including kiosks and street traders.

Mainstream banks have taken up the challenge, widened their countrywide reach, embraced hi-tech like Artificial Intelligence and Machine Learning, and are going all out to prioritise customer satisfaction and trust. Obviously banking stocks are in demand. Corporate India recommends five rewarding banking stocks for prudent investors

The Indian banking sector, with a market value of $ 450 billion and an asset value of $ 2.9 trillion in 2023, is on a growth trajectory, aided by strong economic growth, rising disposable incomes, increasing consumerism and easier access to credit. According to the country’s central bank, the Reserve Bank of India, the sector is sufficiently capitalised and is also well-regulated. At a time when the global banking segment is facing challenges, the Indian banking sector remains unaffected and is on a growth path. In fact, the economic and financial conditions in the country are superior to those in many other countries. Credit, market and liquidity risk studies suggest that Indian banks are generally resilient and have withstood the global downturn well.

Going a step ahead, the Indian banking industry has of late witnessed the roll-out of innovative banking models like payments banks and small finance banks. In recent years, India has also focused on increasing the banking sector’s reach through various schemes like the Pradhan Mantri Jan Dhan Yojana and post office payment banks. Initiatives like these, coupled with major banking sector reforms like digital payments, neo-banking, the rise of Indian non-banking financial companies (NBFCs), and fintech, have significantly enhanced financial inclusion within the country and have helped fuel the credit cycle.

India’s fintech industry is projected to reach $ 150 billion by 2025. By now, the country has emerged as the 3rd largest fintech ecosystem globally. Interestingly, India is one of the fastest growing fintech markets global.

According to IBEF, at present there are more than 2,000 DPIIT (Department for Promotion of Industry and Internal Trade)-recognised financial technology (fintech) businesses in India and this number is rapidly increasingly. The digital payment system in India has evolved the most among a cohort of 25 countries, with the immediate payments service being the only system at level five in the faster payments innovation index (FPII). India’s unified payments interface (UPI) has also revolutionised real-time payments and has strived to increase its global reach in recent years.

The banking sector in India has witnessed several changes over the decades. After then Prime Minister Indira Gandhi nationalised most banks in the 1970s, the sector was dominated by public sector banks. But after the economic liberalisation reforms initiated by Prime Minister Narasimha Rao and his Finance Minister Dr. Manmohan Singh, private sector banks took the opportunity and started competing with public sector banks. In fact, the pace of growth of private banks is the fastest globally.

Today, the figures are: private sector banks 21, public sector banks 13. Additionally, there are 44 foreign banks operating in the country and 12 small finance banks, besides co-operative banks and regional rural banks.

Today, there are around 1.7 lakh bank branches countrywide, making for over 15 branches per 1 lakh population. There are over 2.20 lakh ATMs, with 47% of them in rural and semi-urban areas.

And the banking sector is not lagging behind in terms of innovation and new technologies. Digital payments have substantially increased because of the concerted and coordinated interface between the government and the RBI and all stakeholders. UPI volumes for the first quarter of fiscal 2025 (April-June 2024), have spurted. Not surprisingly, India accounts for nearly 4 per cent of global digital transactions. As on July 31, 2024, there were 602 banks actively using UPI. According to the RBI, deposits of all scheduled banks surged by a whopping Rs 2.11 lakh crore ($ 2.544 billion) as of July 12, 2024.

The remarkable growth of instant digital payments in India has already changed the face of the country’s payments industry, particularly for small-ticket transactions between merchants and customers. “However,” says banking expert Gaurav Mehra, “banks must prepare for a second wave of disruption as both instant payments and embedded finance begin to revolutionise other kinds of financial services and customer journeys.”

In fact, the rest of the world is playing catch-up with the rate of change in India, where a biometric identity scheme launched in 2009 propelled country-wide financial inclusion. Furthermore, the 2016 launch of the revolutionary Unified Payments Interface (UPI), set up by National Payments Corporation of India (NPCI), allows mobile phone users to make instant, fee-free payments and transfers by scanning QR codes. UPI monthly transactions hit 11 billion in October 2023, up from a few hundred million in early 2018, significantly displacing cash across the country at outlets, including kiosks and street traders.

With UPI now linking hundreds of banks and digital payments providers to around 50 million merchants and 300 million customers, banks need to take the initiative in the next wave of change. UPI is set to become a more important platform beyond just person-to-person payments – a UPI credit line offering was launched in September 2023. Meanwhile, financial services are likely to be embedded across an ever-widening range of customer journeys. For example, NPCI has rolled out a programme of vehicle-in-motion toll collection across India’s road network, using radio frequency identification technology (NETC FASTag).

Through 2024 and beyond, embedded finance initiatives may begin to introduce click-free consumer payment across activities such as the weekly shopping trip, eating out and drive-thru restaurants, travel and entertainment. Consumers could soon be activating usage-based financial services such as insurance and currency exchange automatically as they cross borders. By some estimates, embedded finance markets in India will achieve 36.3% annual growth (CAGR) over the next few years. However, as the race to cut the number of clicks in a customer journey becomes a race to remove clicks altogether, banks must innovate to remain relevant.

Apart from the innovation challenges ahead, the Indian banking sector has been growing at a rapid pace - in fact, the fastest in the world day. During the last two decades or so, while global banks had to face severe headwinds with a detrimental financial meltdown forcing several banks to shut shop, Indian banks are now in a position to compete with leading global financial institutions. This is because many of them have become more efficient and streamlined since they were privatised in 1991.

There are several factors that have been driving this fast growth of the Indian banking sector. Primarily, the driving force behind the rapid growth of the banking sector has been the country's strong economic growth, which followed on the game- changing policy of economic liberalisation initiated by the Narasimha RaoManmohan Singh duo. The economy, which was growing at a rate of 3 per cent, moved up quickly to 7 per cent, 8 per cent and even close to 10 per cent. When global economies were facing headwinds, the Indian economy maintained its sustained growth rate. In fact, in recent years it has emerged as the fastest growing economy globally. Banking is a vital component of the country's economy and plays a pivotal role in financial intermediation, credit allocation and economic development.

Secondly, rising disposable incomes of people have given a big push to the growth of the banking industry, as with rapid economic growth, incomes too have started shooting up. This has expanded the number of high middle-class people in the country, besides generating millionaires aplenty. This widespread spurt in income levels has led to obust consumerism. With banks rushing to provide consumer products at attractive instalments, the country's banking culture got a big boost.

Realising that people need greater access to banking services, the industry started opening more branches. This explosion of bank branches played a great role in spreading the banking culture among the public. With the passage of time, bank branches started a transformation process by adopting technology. During the last five years or so, technology adoption in the banking sector has doubled, reaching approximately 28 per cent. Today, fintech has become a vital part of India's banking industry, is poised for a 31% CAGR, and is set to become the third largest globally with a projected value of $ 150 billion and over 2,000 DPIIT-recognised firms. The segment is driven by digital payments, embedded credit products, investment tech, and health as well as life insurance.

Little wonder, traditional banks are losing their marketshare to fintech entities due to the latter's cost-effective provision of information-based products. However, despite challenges like marketshare reduction and operational risks, including frauds, the present scenario also offers banks opportunities for growth and innovation.

Today, India leads in global fintech growth with an 87% acceptance rate, surpassing the global average of 64 per cent.

India's digital payments ecosystem, including UPI, IMPS, RTGS and NEFT, has seen significant evolution. IMPS ranks fifth in the Faster Payments Innovation Index, while UPI leads in real-time payments. Digital payments in India grew by 30.19% in 2021, reflecting increased cashless transactions, with the RBI-DPI(Digital Payments Index) reaching 270.59, up from 207.84 a year earlier.

Artificial Intelligence (AI) and Machine Learning (ML) are transforming the banking sector, with 12% of banks reaching advanced adoption levels. Global banks are recognizing the benefits, such as risk reduction and efficiency gains, with potential cost savings of $ 447 billion by 2023. Banks like Bank of America and HSBC are utilizing AI/ ML for enhanced operations and customer experiences, while Indian banks like SBI, HDFC, ICICI, Axis Bank, Andhra Bank, and Kotak Mahindra Bank are also utilizing AI.

Customer centricity is a vital business strategy that prioritizes customer satisfaction and trust. In India, only 45% of people were 'very satisfied' with their primary banking services in 2018, highlighting the need for improvement in the banking sector. RBI Deputy Governor Swaminathan J emphasized the importance of addressing the root cause of customer complaints, resolution at the first point of contact by equipping frontline staff with authority, tools and training, and combating cybercrime.

Parallel to the rapid growth of the banking sector is the good demand for banking stocks. In fact, banking stocks are very closely linked to the economy as both credit growth and margins are dependent on GDP growth and interest rates.

While the banking sector in India offers remarkable investment opportunities, investors should consider certain factors before making investment decisions in order to get sizeable returns on their investments. Here, we refer to certain situations which investors should take into account before investing in banking stocks.

Headquartered in Mumbai, HDFC Bank is the largest private sector bank in the country in terms of assets, and the world's tenth largest bank by market capitalisation. It is also the third largest company on the Indian stock exchanges. Moreover, it is the sixteenth largest employer in India with over 173,000 employees.

The bank, which started its operations in 1995, has grown in stature after its merger with Times Bank and its parent company HDFC (Housing Development Finance Corporation), its acquisition of Centurion Bank of Punjab, and its 9.99% stake in Ferbine, an entity promoted by the Tata group.

By the end of fiscal 2024, the bank's distribution network included 8,735 branches and 20,938 ATMs, spread throughout 3,836 cities and villages.

The bank has outperformed its large peers in the recent past primarily on account of its relatively better margin and asset quality. Separately, the bank has adopted a strategy to securitize loans, apart from slowing down credit growth and accelerating deposit growth to bring down its LDR to premerger with HDFC levels.

This is a good investment bet as, since its inception, it has delivered a whopping 6,492.11% return and its dividend yield of 0.98% has outperformed the industry average. Its shares with a face value of Re 1 are quoted around Rs 1,865 and, viewed in the context of its performance trends, it is expected to touch Rs 2,000 very soon.

Mumbai-headquartered ICICI Bank is a large private sector multinational bank and financial services entity, engaged in the business of consumer banking, commercial banking, insurance, credit cards, investment banking, mortgage loans, private banking, investment management, asset management, mutual funds, exchange traded funds, index funds, wealth management, stock broking and risk management, among others. The bank offers this wide range of services for retail and corporate customers through various delivery channels and specialised subsidiaries in the areas of investment banking, life and non-life insurance, venture capital and asset management.

The bank is a very large entity, with over 6,587 branches and 17,102 ATMs across India. Internationally, it has a presence in 11 countries, with subsidiaries in the UK and Canada and branches in the US, Singapore, Bahrain, Hong Kong, Qatar, Oman, Dubai, China and South Africa. At the same time, it has representative offices in the United Arab Emirates, Bangladesh, Malaysia and Indonesia. The company's UK subsidiary has also established branches in Belgium and Germany.

Unfortunately, the bank lost some of its reputation due to the reportedly unethical practices of Chanda Kochhar, former Managing Director. But after Sandeep Bakshi took over as MD and CEO, things started changing. The bank started coming into its own and has today emerged as a leading growth-oriented private sector bank with a robust financial performance. During the last 12 years, its revenues have more than trebled, from Rs 44,885 crore in fiscal 2013 to Rs 159,516 crore in fiscal 2024, with the profit at net level shooting up more than four and a half times -- from Rs 10,130 crore to Rs 46,081 crore. Prospects for the company are all the more promising, going ahead. In the first half of the current fiscal between April and September 2024, revenues on a standalone basis have amounted to Rs 79,533 crore, as compared to Rs 68,246 crore in the corresponding halftime a year ago, with net profit moving up from Rs 19,909 crore to Rs 22,804 crore.

Today, the bank is relatively well-positioned as it continues to outperform its peers on most parameters, exhibiting strong franchise strength. Thus, its current valuation premium to peers is likely to sustain. Following the announcement of the Q2FY25 results, the stock price on October 29, 2024 moved up over 3 per cent to Rs 1,329.75.

According to Market Mojo, a leading stock analysis platform, the bank's stock has been given a 'BUY' rating. The stock has also been a part of Mojo stocks since January 2024, indicating its consistent performance. Technically, the stock is trading higher than its 5-day, 20-day, 50-day, 100-day and 200-day moving averages, indicating a positive trend in its performance.

In comparison to the Sensex, the stock has outperformed the former with a one-day performance of 3.12% versus the Sensex's 0.41%. In the last month, the stock has also performed better than the Sensex with a 2.03% increase while the Sensex has seen a decline of 6.13%. Overall, ICICI Bank's stock has shown a strong and consistent performance, making it a favourable choice for investors. With its positive movement and outperform tor and the Sensex, it is definitely a stock to watch out for in the banking space.

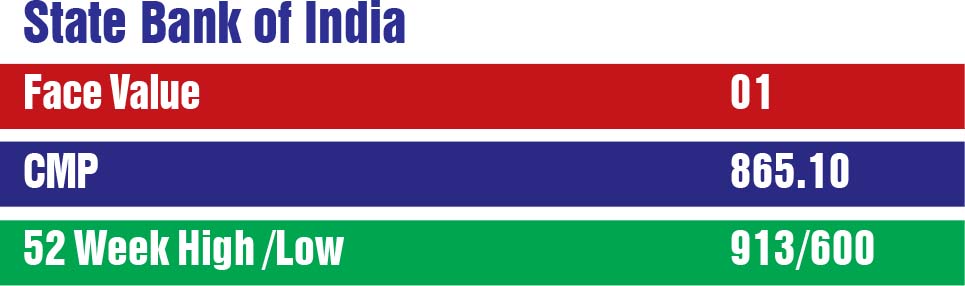

Mumbai-headquartered State Bank of India, the leading commercial bank in the country, is an Indian multinational public sector bank and financial services statutory body. It is the 48th largest bank in the world by total assets and is ranked 78th in the Fortune Global 500 list of the world's biggest corporations in 2024, being the only Indian bank in the list. It is the largest bank in India with a 23 per cent and 25 per cent share of the total loan and deposits market. It is also the tenth largest employer in the country with nearly 250,000 employees (2024). 'Global Finance' magazine has named SBI the 'Best Bank in India' for 2024.

This giant banking entity is engaged in retail banking, corporate banking, investment banking, mortgage loans, private banking, wealth management, risk management, investment management, mutual funds, exchange traded funds, index funds, credit cards and insurance, among others. It has specialised subsidiaries, including SBI Life Insurance, SBI Mutual Fund, SBI Cards and Payment Services, Yes Bank, Andhra Pradesh Gramin Vikas Bank, Kaveri Gramina Bank and Uttarakhand Gramin Bank.

The bank is doing very well on the financial front. During the last 12 years, its revenues have expanded more than two and a half times -- from Rs 167,976 crore in fiscal 2013 to Rs 439,189 crore in fiscal 2024, with the profit at net level spurting over three and a half times -- from Rs 18,555 crore to Rs 69,543 crore.

In September 2022, SBI emerged as the third largest lender after HDFC and ICICI Bank, and the seventh Indian company to cross the Rs 5 trillion (Rs 5 lakh crore) market capitalisation mark on the Indian stock exchanges for the first time. The largest public lender in the country reached a milestone in April 2024 when its market capitalisation surpassed Rs 7 trillion, making it the second public sector undertaking to do so after LIC. In June 2024, the bank crossed an all-time high market capitalisation of Rs 8 trillion, becoming the 7th Indian company to cross this milestone.

Today, SBI stands tall among the best performing banks globally. So far, it has delivered a strong all-round performance and has achieved new milestones in profitability, with net profit surpassing Rs 600 billion in 2024. The current size of its balance sheet at Rs 62 trillion is more than the combined GDP of almost 174 countries in the world. The bank has demonstrated high agility and superior execution even at this huge size, and is well poised to maintain this momentum.

Motilal Oswal, a leading brokerage house, has estimated that SBI will deliver a 16% CAGR in earnings over fiscal years 24-26, backed by healthy loan growth, moderation in opex ratios and controlled credit cost, thus resulting in a FY26 RoA/RoE of 1.1%/18.5%. Motilal Oswal reiterates its 'BUY' rating with a larger price of Rs 1,015.

According to Motilal Oswal, despite already delivering impressive returns over prior years, SBI's consistent performance in RoE and its leadership position in key operating metrics will enable the bank to deliver strong returns going ahead. As India progresses towards its goal of becoming a developed nation by 2047, SBI's strong return ratios and healthy grown momentum should keep investor interest in the bank intact, potentially elevating its position in the global rankings and solidifying its status as a compelling investment opportunity.

The bank remains well-positioned to deliver sustainable growth with high profitability led by healthy loan growth, controlled opex and provisions, and technological advances. Little wonder, the management has guided for broadly stable margins going forward as the bank has measures in place to mitigate the impact of the elevated cost of deposits. According to Motilal Oswal, the bank is well-positioned to sustain its growth trajectory, supported by a low CD ratio, strong underwriting and continued momentum in YONO. The asset quality performance remains strong, with consistent improvement in asset quality ratios.

Its shares are quoted around Rs 865. Most analysts expect the price to cross the Rs 1,000 mark within a year or so Kotak Mahindra Bank is another of India's leading private sector banks, with a network of over 1,600 branches and 2,600 ATMs nationwide.

The bank, which was established in 1985 as Kotak Mahindra Finance Limited, a non-banking financial company, in 2003 was converted into a bank. Since then, it has grown rapidly through organic and inorganic expansion, acquiring several businesses such as ING Vysya Bank, BSS Microfinance, and Ford Credit India. But why is this stock worth investing in? Check out the pointers.

Bandhan Bank has a network of over 6,000 banking outlets and 438 ATMs across 35 states and union territories. Over 3.26 crore customers trust this bank's service. Bandhan Bank is also firmly committed to social responsibility, with its Corporate Social Responsibility (CSR )programmes reaching out to more than 19 lakh participants in 13 states, focusing on education, health, livelihood, and women empowerment. The bank started 2001 as a microfinance institution and became a full-fledged bank in 2015. But why is this stock worth investing in? Check out the pointers.

April 15, 2025 - First Issue

Industry Review

VOL XVI - 13

April 01-15, 2025

Want to Subscribe?

Read Corporate India and add to your Business Intelligence

![]() Unlock Unlimited Access

Unlock Unlimited Access

Lighter Vein

1 Year *

Subscription

Rs 2400 /-

3 Year *

Subscription

Rs 6000 /-

5 Year *

Subscription

Rs 9000 /-

5

International

Subscription

$ 99.99

Read Corporate India and add to your Business Intelligence

Popular Stories

A modern-day enigma and a ramification of humanity's never-ending advancements, e-waste refers to the scum con- cealed by the outward glow of ever-advancing technology.

Archives

Office Address

Unit No. 405, 4th floor, Madhu Industrial Park, Avadh Narayan Tiwari Marg, Mogra Village Road, Andheri (East), Mumbai – 400069.

Call/Whatsapp

If you are interested in advertising with Corporate India, please don't hesitate to contact us. Our team is here to assist you with the process and answer any questions you may have. We look forward to the opportunity to work with you and help your business reach its full potential.

Fill out the form below to subscribe to our newsletter and never miss an update